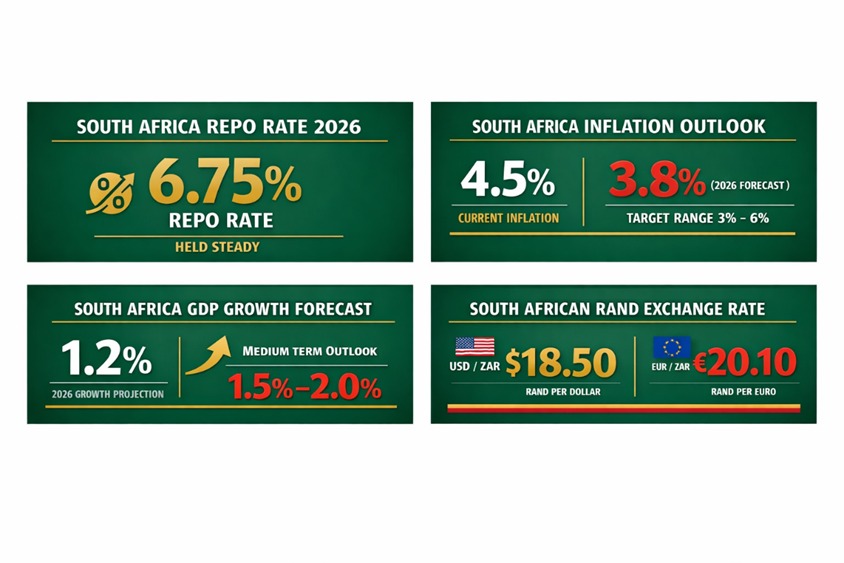

The South African Reserve Bank (SARB), opted to hold its benchmark repo rate at 6.75 per cent at its first monetary policy meeting of 2026, a decision that highlights the cautious balance policymakers are striking between inflation control and economic support. The Monetary Policy Committee (MPC) was not unanimous: four of six members voted to maintain the rate, while two favoured a 25-basis-point cut, underscoring the nuanced debate within the bank about the appropriate stance of monetary policy in an evolving economic context.

The SARB’s policy framework remains centred on maintaining price stability, with the official inflation target now focused on 3 per cent following a policy adjustment in late 2025. This narrower and lower target reflects a commitment to anchoring expectations in a world where global price pressures have been volatile, even as headline inflation in South Africa has moderated. In December 2025, headline consumer price inflation rose slightly to 3.6 per cent, marginally above the new target but broadly within the bank’s tolerance parameters.

READ ALSO: South Africa’s Automotive Rebirth: Can New Policy Deliver Competitive Revival?

Governor Lesetja Kganyago and the MPC emphasised in their announcement that inflation expectations have declined, with longer-term expectations at historically low levels. This was highlighted as an important element in ensuring inflation converges to the 3 per cent target over the coming years, potentially by 2028, according to SARB’s projections.

Despite this progress, several domestic and external inflationary risks persist. The outbreak of foot-and-mouth disease has exerted upward pressure on meat prices, while uncertainty around electricity tariffs, with potential corrections rising from R54 billion to R76 billion, represents a material risk to the inflation outlook. Global geopolitical tensions, elevated public debt levels in advanced economies, and safe-haven flows into commodities such as gold add to the backdrop of uncertainty that the MPC must navigate.

Growth Prospects and the Policy Tightrope

The SARB’s decision to hold rates was taken against a backdrop of modest expansion in South Africa’s economy. Official projections have placed real GDP growth at around 1.4 per cent in 2026, with a gradual improvement to 1.9 per cent in 2027, reflecting cautious optimism about domestic demand and investment dynamics.

This subdued growth outlook is characteristic of many emerging markets currently negotiating the legacy of global tightening cycles with the need to stimulate domestic activity. While a stronger currency, the South African rand recently reached levels around R15.80 to the dollar for the first time since mid-2022 has helped moderate import costs and inflation pressures, it also complicates the competitive dynamics for exports in an uncertain global demand environment.

Within this context, the split vote among MPC members reflects differing interpretations of the balance between supporting economic activity and ensuring inflation decisively returns to target. Those favouring a rate cut emphasise the easing inflation trajectory and subdued growth; those supporting the hold underscore the importance of verifying that inflation expectations remain firmly anchored and that emerging risks do not compromise price stability.

South Africa’s cautious stance is not occurring in isolation. Across both advanced and emerging markets, central banks are navigating divergent macroeconomic pressures. In contrast to expectations of potential rate cuts in countries such as Brazil and Nigeria, major economies such as Canada, Japan, and Switzerland are contemplating or have implemented higher-for-longer policy rates, while others like Australia and New Zealand are actively trimming borrowing costs. These international divergences underscore the complex interdependence of monetary policy, capital flows, and exchange rate dynamics in a world still adjusting to post-pandemic and post-geopolitical shock realities.

For sub-Saharan Africa in particular, the SARB’s policy choices have spillover effects. As Africa’s largest economy, South Africa’s interest rate trajectory influences regional capital flows, borrowing costs and investor sentiment. A sustained period of stable policy, whether by holding or gradually easing rates, can shape funding conditions in neighbouring markets, affect cross-border investment, and set benchmarks for monetary conditions across the continent.

Forward Guidance and Policy Outlook

Looking ahead, the SARB has made clear that policy adjustments will continue to be data-dependent, assessed on a meeting-by-meeting basis. The Quarterly Projection Model published by the bank continues to forecast gradual rate cuts as inflation subsides, but with significant caveats built into alternative scenarios. In a favourable environment, including a stronger rand and lower energy prices, inflation could dip as low as around 2.3 per cent temporarily, creating scope for earlier easing. By contrast, adverse conditions could see inflation linger near 4 per cent, delaying cuts and extending the period of moderately restrictive policy.

The nuanced split in the MPC vote underscores a central bank attuned to the shifting interplay between price stability and growth. For global investors, policymakers and financial markets, the SARB’s approach in 2026 will be closely watched not just for South Africa’s macroeconomic trajectory, but for its broader implications for emerging market monetary policy frameworks in an increasingly uncertain global environment.